Assessing portfolio risks is never straightforward, and extreme asset moves can negatively impact portfolios in ways which may not be captured by conventional risk measures [1]. If diversification breaks down portfolio values may not be protected. Stress-testing can be used to estimate portfolio impacts, typically looking at historical market events or artificial scenarios. The pros and cons of these approaches are discussed in [2]. This article summarises the results of historical stress-testing applied to P1’s Hybrid model portfolios at the end of March 2017. Stress-testing is periodically carried out on P1’s models, and further testing has been carried out since then; however, the March 2017 results can now be released.

Historical stress-testing

Historical stress-testing uses scenarios over intervals when assets performed poorly. Asset price behaviours are applied to portfolios to see how they would respond. The periods were deliberately selected to be challenging, with adverse impacts on portfolio values; indeed, a scenario is not a stress-test unless the outcome is adverse [1]. However, historical events may not be a reliable guide to the future, so while stress-tests can help quantify risks, they do not resolve them. Although stress-testing cannot be guaranteed to identify the actual impacts of future events on a portfolio, they represent another tool in the risk manager’s armoury.

Scenarios

Broadly stress-test scenarios should have negative consequences and be regarded as “unlikely but plausible” [3]. P1 identified eight historical scenarios of primary concern, and which would have a negative impact on the Hybrid models. These included the 9-11 September 2001 World Trade Centre attacks, Black Monday, the 2015 Chinese Stock Market Crash, the Dot-com bubble, the 2010 European Sovereign Debt Crisis and the 2008 Financial Crisis.

During stress-testing, it is good practice to permit no model rebalancing, even for extended scenarios. By using the model weights prevalent at the time, this made the tests forward-looking. The worst losses during each of the scenario periods for the P1 Hybrid models are shown in figure 1.

| Figure 1: P1 Hybrid Model Stress-tests. Risk levels from lowest risk (P1 Cautious) to highest risk (P1 Adventurous). |

Almost without exception, the results show that the worst losses associated with each P1 Hybrid model increased with the model risk level. As model risk level increased, so did the loss from each adverse scenario. This is reassuring since it implies that the relative risk rankings of the models are as intended, even though abnormal market conditions have been applied.

The exception is for the Financial Crisis stress-test, where the loss associated with the Adventurous model was slightly less than that of the Moderate-Adventurous model. This is explained by the differing asset allocations between the two models. The Financial Crisis had a much more significant impact on property values than the other tests. Apart from a lower property allocation, the Adventurous model also had higher exposure to overseas equity than the Moderate-Adventurous model which ameliorated the outcome.

Recovery time

After a market crisis, investors are concerned about how quickly their portfolios will recover their previous values. Lower-risk portfolios would be expected to recover more rapidly than higher-risk portfolios. In all the above scenarios the P1 models recovered their previous values, but how quickly?

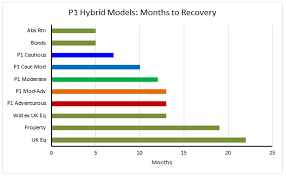

Figure 2 shows the recovery times for P1 Hybrid models during the Financial Crisis stress-test. The highest risk-profile models took longer to recover than the lower risk models, precisely as would be expected. For context, the figure also shows the recovery times associated with other asset classes based on index returns. For this scenario, while UK equities took 22 months to recover, the highest-risk P1 model took only 13 months, just over 1 year; while P1’s lowest risk models recovered in only 7 months.

|

| Figure 2: P1 Hybrid Model recovery times for Financial Crisis stress-test scenario. Risk levels from lowest risk (P1 Cautious) to highest risk (P1 Adventurous). Also shown are asset class recovery times represented by indices. |

Overall P1 Hybrid Model risk levels

Although these results only represent one way of looking at P1 Hybrid model risks, they are very reassuring. Conventional risk methodologies had already been used to define the profiles. When unconventional risks were applied to the models, using the historical stress-test scenarios above, the P1 Hybrid models responded as would be expected. Under extreme situations representing challenging market conditions, the lower-risk models had smaller losses than higher-risk models, with only one exception for a single scenario. This was when the P1 Adventurous model proved more protective than might have been expected during the 2008 Financial Crisis scenario.

Furthermore, the results also showed that for the Financial Crisis scenario the P1 Hybrid models recovered in only 7-13 months, much more quickly than UK equities, which took 22 months. Again, lower risk models recovered more rapidly than higher-risk models, as would be expected.

How this helps Advisers

It is vital that advisers should be able to discuss investment risks with their clients, including for extreme market events. Advisers also need to be confident that wealth managers are correctly addressing non-conventional risks and the possibility of market crises. P1 Investment Management’s stress-testing programme addresses both concerns. Being able to discuss market crises with clients provides a robust framework for better client conversations. Clients and advisers can also gain a realistic idea of how long portfolios may take to recover and how these may compare across asset classes. The stress-testing programme should also reassure advisers that P1 is working hard to address a wide variety of risks within client portfolios, to best support its clients.

References

| [1] | Q. G. Rayer, “Dissecting portfolio stress-testing,” The Review of Financial Markets, vol. 7, pp. 2-7, 2015. |

| [2] | Q. G. Rayer, “Managing risk: stress-testing investment portfolios.,” DISCUS, 26 January 2017. [Online]. Available: http://discus.org.uk/managing-risk-stress-testing-investment-portfolios/. |

| [3] | M. Crouhy, D. Galai and R. Mark, The essentials of risk management, 2nd ed., New York: McGraw-Hill Education, 2014. |